Following the flow: Tracking the who, what and where of Industrial Strategy investment

Context

In June 2025, government published its Modern National Industrial Strategy, a “10-year plan to deliver the certainty and stability businesses need to invest in the high growth sectors that will drive our growth mission”. As part of this, 8 priority sectors were identified (IS-8) as key industries that are expected to drive national productivity, innovation and long-term economic growth. These sectors included Advanced Manufacturing, Clean Energy, Creative Industries, Defence, Digital & Technologies, Financial Services, Life Sciences, and Professional & Business Services.

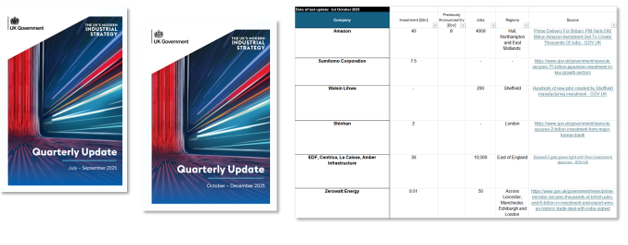

In September 2025, The Department for Business and Trade published the first quarterly update on the delivery of its Modern Industrial Strategy, covering the performance of the IS-8 in terms of key delivery milestones, policy and economic metrics. Alongside these, a more granular breakdown of the investments landing across them is published, covering major investment projects where government has been involved in the process or where they stem from policy decisions made as part of the Industrial Strategy. Since then, there has been one update in January.

The material within the updates provides a helpful, broad overview. But, for us, it doesn’t go far enough in explaining what this activity means for places, for their growth, or for the real-world dynamics shaping sectors on the ground locally. That gap is precisely where Metro Dynamics’ real interest begins.

Why we’re doing this and why it matters

We have built on list of investments and headline overview documents, undertaking additional research to understand the nature of the investments to provide further insights for our work in places. We wanted to know:

WHO are the actors shaping growth? So, we’ve collected extra information on which investors, firms and partnerships are involved and where they are largely based.

WHAT type of activity is taking place? So, we’ve looked to captured more detail and categorised to distinguish between investments’ core focuses E.g. between R&D, or expansion or scale-up activity.

And critically for Metro Dynamics…

WHERE is investment actually landing, and how does that connect with the local economy and existing or emerging clusters? So, we’ve further built out information on investment location.

This work builds on our previous analysis of the IS8 sectors within the Sector Growth Index, layering how investment and policy activity are actually playing out on the ground.

Metro Dynamics Sector Growth Index Dashboard

What does the first Following the Flow briefing show?

Are we seeing the frontier-level growth, re-shaped economic landscape and new industrial capabilities that the Industrial Strategy is aiming for? Only time will truly tell, but in the first two quarters we can see…

Corporate-led expansion dominating over new capital formation. The majority of commitments so far reflect firms scaling and modernising UK operations, suggesting deepening of value chains rather than wholesale industrial reinvention.

A clear sequencing of transformation: backbone infrastructure first, ecosystem expansion second. Large-scale commitments in AI, energy and advanced manufacturing, followed by a broader wave of innovation-led and capability-building projects.

Digital and Clean Energy acting as enabling platforms across the IS-8. These sectors are not just beneficiaries of investment, they are shaping the conditions for growth in the others.

The acceleration of existing strengths, more than creating new geographies of growth. Investment so far is reinforcing established hubs and corporate footprints rather than fundamentally redistributing economic activity.

This early activity suggests the Industrial Strategy is amplifying the UK’s existing economic architecture and deepening its strongest ecosystems first. While rational, this risks widening gaps unless places with high potential, but currently less developed systems, are actively supported to build capability and attract follow-on investment.

What next?

We await the next update. In the meantime, alongside the overarching perspective on investment trends, we’re developing a series of sector‑specific spotlights. This is about creating an evolving, responsive, commentary and tracking resource that places and partners can use to gain a stronger insight into the IS-8 and the investment that is following it now and into the future.

Overall reflections

Who?

The UK is attracting a broad and diverse mix of investors, ranging from global corporates and high‑growth technology firms to major energy utilities, manufacturing leaders, creative‑tech studios, and financial institutions.

These sit alongside a smaller number of VC or PE, sovereign‑backed actors and both UK and overseas pension funds. The majority are corporates investing directly into their own UK expansion.

Investment is arriving from a globally diverse set of firms spanning the US, India, Europe, Japan and the Middle East, most of which already have substantial UK footprints. Their latest commitments therefore represent deepening and modernisation of UK operations rather than purely new ‘inbound’ foreign investment.

What?

The investments show both depth and breadth: Transformational mega‑investments are complemented by a diverse pipeline of R&D‑oriented and market‑expanding activity that strengthens the competitiveness and broader ecosystems of the IS-8 sectors in the UK.

Digital and Technology remains the single most active area of activity, but Advanced Manufacturing, Clean Energy, Financial Services, Creative Tech, and Professional Services all feature in substantive ways.

What stands out is the combination of system‑level investments, such as data centres, energy infrastructure, advanced manufacturing facilities, and AI compute capacity, with a rich pipeline of innovation‑led and capability‑building projects, particularly in software, analytics, cybersecurity, fintech, and AI‑enabled services.

Where?

Investment continues to flow into the established hubs such as London, the South East, West Midlands, North West although there is a notably large sample of investments which are ‘place agnostic’ (no place assigned within official releases) which is important for considering how place-based the focus is currently.

Focus on Q3 2025 (July-September)

Based on n=49 provided investments

Who?

Investment was predominantly from firms with HQ/established presence across US and Europe, particularly in cloud, data centres, energy systems, and large‑scale manufacturing, with a flow of activity from several high‑growth technology and services companies headquartered in India who are steadily building their UK delivery and innovation presence.

What?

Between July and September, investment activity was shaped by a smaller number of projects that carried significant strategic weight. This period was dominated by Digital & Technology and Financial Services, with Clean Energy forming a strong third pillar with fewer but much larger, infrastructure‑heavy commitments.

A defining feature of the quarter was the presence of several large, platform‑shaping commitments from global firms with deep existing UK footprints and investments that expanded the UK’s long‑term industrial and technological backbone, from AI, cloud and data‑centre capacity to energy systems spanning nuclear, renewables and grid‑related upgrades. A small number of “mega commitments” (e.g. Amazon, Microsoft, Sizewell C, Iberdrola, Blackstone) drove the aggregate value.

Where?

Investments were split between a sizeable set of “place agnostic” commitments and a strong London-led concentration of place-specific activity. Beyond the capital, the quarter shows a thin but strategically important tail of investments landing across a small number of other places (e.g., Scotland, Manchester, Edinburgh, Hertfordshire, East of England, Hull) and a handful of explicitly multi-place footprints (for example, one investment spanning across various parts of the North and Scotland), suggesting that several of the largest or most operationally significant projects were framed as national or networked deployments rather than single-site bets.

Focus on Q4 2025 (October-December)

Based on n=94 provided investments

Who?

Rather than being driven by a handful of mega‑projects, the quarter is characterised by a large number of corporates investing directly into their own UK expansion, with a strong focus on R&D centres and technology‑driven capability growth across multiple sectors.

What?

Between October and December we see a broader wave of mid‑sized, innovation‑oriented projects. While there are still major infrastructure and energy commitments, the quarter is especially rich in AI and cloud infrastructure, cybersecurity, software and data‑platform development, offshore wind and clean‑energy upgrades, advanced manufacturing technologies, and creative‑tech production facilities.

This quarter shifts the pattern from Q3. The volume of activity rises sharply and the sectoral footprint widens. Investments land across a variety of regions, reflecting a more distributed phase and the tone of the quarter is one of breadth, dynamism and capability-building, complementing the large-scale structural bets laid down earlier in the year.

Where?

By Oct–Dec, the pattern becomes more distributed across UK regions and nations, while still retaining a clear London hub for place-specific announcements. “Place agnostic” entries remain prominent, but among the investments that do specify a location, there is a broader spread across Wales, the North West, West Midlands, East Midlands, Scotland, the East of England, the South East, South West, and Northern Ireland, a materially wider geographic mix than the prior quarter. The overall impression is of a quarter where investment activity is simultaneously centrally anchored in Greater London for many business-facing, digital and services-oriented moves, and increasingly multi-regional for industrial and infrastructure projects.

What next?

We await the next update. In the meantime, alongside the overarching perspective on investment trends, we’re developing a series of sector‑specific spotlights. This is about creating an evolving, responsive, commentary and tracking resource that places and partners can use to gain a stronger insight into the IS-8 and the investment that is following it now and into the future.

To explore our interactive dashboard to see where investments are landing across places and to understand their value and scale of impact – get in touch with fiona.tuck@metrodynamics.co.uk or ben.jones@metrodynamics.co.uk

Method note: IS-8 categorisations of investors/projects have been done manually as best-fit given the absence of this information within the DBT release, using categorisations across more than one sector where relevant. Locations of where investment is landing were provided in some cases in the DBT release, but these have also been built on where additional information could be found.