Is Manchester’s economy finally taking off?

This is an abbreviated version of an article originally published on the Manchester Mill, a leading regional newspaper, by James Gilmour, a Senior Consultant at Metro Dynamics. You can subscribe to the Mill here.

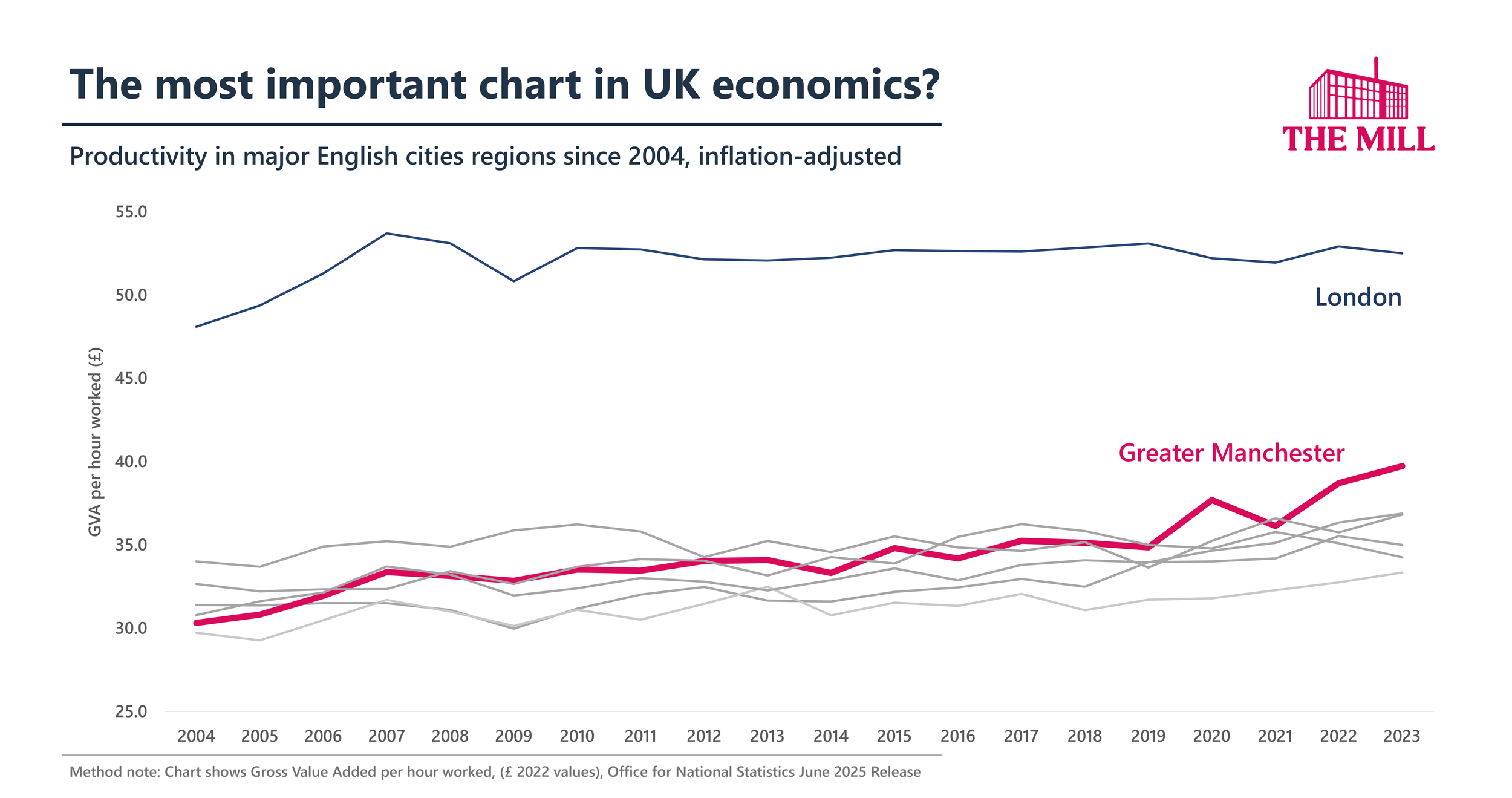

I want to make the case that what follows is the most important chart in UK economics. I think it tells us that something different genuinely is happening here in Manchester, or maybe that something isn’t happening elsewhere that should be. And it might give us a hint as to how to solve the biggest challenge of UK economic policy – one that’s left us all thousands of pounds worse off.

Unhelpful jargon

The first thing to understand about “productivity” is that it has nothing to do with productivity. Bear with me.

“Productivity” is a measure of how effectively we’re able to turn our time into economic value. It’s less about how hard we work, than about the tools we have available, the methods we use – and how much the rest of the world values what we do.

For example, I would have to work phenomenally hard to craft a single paperclip. But in a world where a machine can produce thousands of identical paperclips every minute, I would have wasted my time. My paperclip might be of sentimental value to my beloved friends and family, but I’m unlikely to win a lucrative contract to supply WHSmith.

So when the data tells us that Manchester is more productive than, say, Sheffield, it’s not to say Mancunians are demonstrating their industrious nature against the easy-going folk of Yorkshire. In fact, it’s probably the opposite; the “highest value” jobs in the modern economy are some of the most pleasant, varied and intellectually engaging, compared to the draining emotional labour of customer-facing retail, the monotony of machine-line production, or the always-on tension of the gig economy.

Economists love productivity. The higher productivity goes, the more money there is to go around. Wages can rise while prices fall. Unfortunately for the British, our productivity has been almost flat since the 2008 financial crisis; this makes us something of an international outlier and has been described as the “productivity puzzle”, as nobody has yet quite figured out why this has happened (on which more later).

In 2004 – when this data first began to be collected, and when talk of Manchester’s booming economy started to become commonplace – Greater Manchester (GM) was bumping along at the bottom of the pack, and productivity was 89% of the UK average. Fast forward to the latest data in 2023, and productivity is up to 97% of the UK average, powered by chunky and consistent productivity growth in Manchester over the last decade.

This is big news. For decades, we’ve been told that the UK’s second cities punch below their weight, and that’s holding back the prosperity of our regions (side note – generally speaking, bigger cities tend to be more productive, as size allows for variety and specialisation, among a raft of other factors known loosely as agglomeration).

Did Manchester do things differently here?

So it’s simple then. We figure out what worked in Manchester, we roll it out across the country – keeping the good parts and ditching the gimmick bars and eye-watering rent increases – and we all get rich.

Unfortunately, there’s no smoking gun. Productivity is associated with a range of factors, ranging from the skills of workers to the level of investment in their equipment. Even leading academics struggle to attribute more than half of the difference between places to the factors we can observe (handily chalking up the gaps in their sums to something called “Total Factor Productivity”).

A lot has happened in GM, but one of the most distinctive things this city has seen is rapid growth in jobs based in the city centre. The inner city has also become much more important as a centre for employment for the wider city region, with Manchester hosting 31% of all jobs in GM (up from 25% in 2004).

Those city centre jobs are, increasingly, those in the high-end professional services that the UK has a distinctive niche in. Law, consultancy, media; these jobs are highly productive, they generally pay well, and they benefit from proximity, favouring the clustering possible in the city centres. They also have high barriers to entry, requiring not only that you live in a place with good access to those jobs, but that you have the necessary qualifications and social capital.

This trend, to be clear, is happening pretty much everywhere; city centre growth is part of the bargain of the transition to services our country struck in the 1980s. But in Manchester, this process was supercharged in the mid-2010s, when it began rapidly outpacing the other big cities in terms of job creation in the inner city:

Concurrently (although possibly not coincidentally), the early 2010s saw the completion of the massive Phase 3 Metrolink expansion. This was the expansion that, give or take a line, created the mass transit network we have today, and was swiftly followed by an explosion in passenger numbers right up until the pandemic.

It may not be definitive proof, but when academic after academic tells us that poor public transport is holding back the economies of our regional cities, it certainly seems like having a moderate level of investment in infrastructure didn’t hurt.

I could be completely wrong. But given how much money is riding on this, I definitely shouldn’t be the only person speculating. Yes, we did things differently here, but which bits mattered? It’s in all of our interests to find out.